Normal Distribution

- Pr(y∣μ,σ2)=2πσ1e−2σ2(y−μ)2

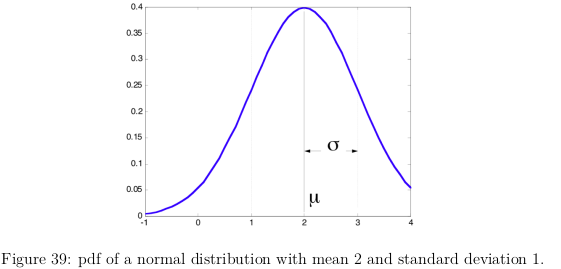

- Mean μ and std σ. μ is max and μ±σ is locations of zeros of second derivative

- N(0,1)

- Central Limit Theorem

Properties

- Linear combinations of normal distributed independant RVs are normal distributed

- X,Y have means μ and v and variances σ2 and τ2. Then aX+bY is normally distributed and has mean : aμ+bv and variance α2σ2+b2τ2

Computing the Value

- ∫ab2πσ1e−2σ2(x−μ)2dx

- Transform N(μ,σ2) to N(0,1)

- Z=σX−μ

- ∫σa−μσb−μ2π1e−2(x)2dx

- Compute by using Cumulative Density function ϕ

- Iterative solvers

- ϕ(σb−μ)−ϕ(σa−μ)

- μ^=N1Σi(xi) σ^2=N−11Σi(xi−μ^)2